5 Simple Techniques For How Much Do Dentures Cost Without Insurance</h1><h1 style="clear:both" id="content-section-0">The 2-Minute Rule for How Much Home Insurance Do I Need

If you presume that elements of your home are not up to present building codes, consider getting a recommendation to your policy called an Ordinance or Law, which pays a defined quantity towards bringing a home up to code during a covered repair work. Lovely, unique functions on older homeslike wall and ceiling moldings and carvingsare expensive to recreate and some insurer may not offer replacement policies because of that.

This suggests that rather of fixing or changing features normal of older homeslike plaster wallswith like products, the policy will pay for repairs utilizing today's standard building products and construction techniques. Inflation can affect restoring expenses. If you intend on owning your home for a while, think about adding an inflation guard stipulation to your policy.

After a significant catastrophe such as a cyclone or Go to this site twister, building expenses might rise all of a sudden because the price of building products and building employees increase due to the extensive demand. This rate bump may press rebuilding expenses above your homeowners policy limitations and leave you short. To secure against this possibility, an ensured replacement cost policy will pay whatever it costs to rebuild your house as it was prior to the disaster.

The majority of homeowners insurance policies supply protection for your possessions at about 50 to 70 percent of the insurance coverage on your residence. Nevertheless, that standard quantity might or may not be enough. To find out if you have enough coverage: In order to precisely evaluate the worth of what you own, it's extremely suggested to perform a house stock.

In case any or all of your things is stolen or harmed by a disaster a stock will make filing a claim much simpler. There are a number of apps offered to help you take a house stock, and our post on how to create a home stock can help, also.

The How Much Does Health Insurance Cost Per Month Ideas

The cost of replacement cost coverage for homeowners has to do with 10 percent more but is typically a rewarding investment in the long run. (Note that flood insurance coverage for valuables is only offered on a real cash worth basis.) If you think you need more coverage, call your insurance coverage expert and ask about greater limits for your personal ownerships.

For instance, jewelry coverage might be limited to under $2,000. Some insurer may likewise position a limit on what they will spend for computers. Inspect your policy (or ask your insurance coverage expert) for the limits of your protection for any costly products. If your home inventory consists of products for which the limits are too low, consider purchasing a special personal residential or commercial property floater or a recommendation.

Extra Living Expenses (ALE) is a really important feature of a standard house owners insurance plan. If you can't reside in your house due to a fire, serious storm or other insured catastrophe, ALE pays the extra expenses of temporarily living elsewhere. It covers hotel costs, dining establishment meals and other living costs sustained while your house is being reconstructed.

Lots of policies offer protection for about 20 percent of the insurance on your house. However ALE protection limits vary from company to business. For example, there are policies http://elliottncqp487.cavandoragh.org/what-does-how-much-is-health-insurance-a-month-do-h1-h1-style-clear-both-id-content-section-0-not-known-details-about-how-to-get-rid-of-mortgage-insurance that provide an unrestricted amount of coverage, for a minimal quantity of time, while others might only set limits on the amount of coverage.

The liability portion of property owners insurance covers you versus claims for bodily injury or property damage that you or member of the family or family pets trigger to other individuals, as well as court costs sustained and damages awarded. You should have sufficient liability insurance coverage to protect your assets. Many house owners insurance plan offer a minimum of $100,000 worth of liability insurance coverage, but higher quantities are available and, increasingly, it is suggested that house owners think about acquiring a minimum of $300,000 to $500,000 worth of liability protection.

Not known Facts About How Much Does It Cost To Go To The Dentist Without Insurance

Umbrella or excess liability policies offer coverage over and above your standard home (or automobile) liability policy limits. These policies begin to pay after you have consumed the liability Helpful resources insurance coverage in your underlying policy. In addition to providing additional dollar quantity coverage, umbrella or excess liability typically offers more comprehensive protection than basic policies.

The greater the underlying liability protection you have, the more affordable the umbrella or excess policy. To compose an umbrella or excess policy, the majority of companies will need a minimum of $300,000 underlying liability insurance on your basic property owners policy.

If you own a house, you might question just how much homeowners insurance you really need. After all, the more protection you have, the greater the premiumsand you probably desire to avoid paying more than you require to. Still, if you don't have sufficient protection, could you manage to reconstruct your home and change your personal belongings if a disaster were to strike? The bright side is that you can tweak your property owners insurance coverage to ensure you have the ideal typeand right amountof protection.

Standard policies do not cover whatever, so you might need extra protection to secure against hazards such as floods and other natural disasters. Your insurance coverage representative can help you choose the type and amount of coverage you require. A house is likely the largest single purchase you'll ever make, so it makes good sense that you would wish to safeguard that financial investment.

Another way is to purchase an excellent property owners insurance policy. Homeowners insurance is a type of property insurance coverage that safeguards your house and other valuable items. A basic policy covers damage and losses to your house and individual belongings. It likewise safeguards your possessions from liability claims, such as injuries and pet-related events.

How How Much Does Long Term Care Insurance Cost can Save You Time, Stress, and Money.

According to the Insurance Coverage Information Institute, a few of the most common dangers covered by standard homeowners policies include: Damage from an airplane, cars and truck, or vehicleExplosionsFalling objectsFire and smokeLightning strikesRiots or civil commotionTheftVandalism and malicious mischiefVolcanic eruptionsWater damage (from within the home only) Weight of ice, snow, and sleetWindstorms and hail The portion of homeowners who incorrectly think flood damage is covered by their standard policy, according to Princeton Survey Research Associates International Source: How Insurance Misconceptions Can Expense You While basic policies cover many different dangers, they don't cover whatever, consisting of: Flood insurance is specifically omitted from basic policies, so you need to buy it as a different policy.

involve some type of flooding. how many americans don't have health insurance. Earthquake coverage is normally available as a different policy or as an endorsement to your existing house owner's protection. Homeowner's insurance coverage doesn't cover mold, invasion from termites and other pests, or damage due to absence of upkeep. Sewage system backups aren't covered by standard policies or by flood insurance.

According to Insurance coverage. com, if you have a mortgage, your loan provider will require a minimum quantity of dwelling and liability coverage. That protection protects your investmentas well as your lending institution's. About 60% of all homes in the U.S. are underinsuredby approximately 20% according to a report from housing information company CoreLogic.

Getting My How To Get A Breast Pump Through Insurance To Work

Meanwhile, once you discover the insurance provider, contact them to see if the policy is still active. If it is, the insurance company has actions you can follow to submit a claim. It's crucial to follow these directions closely as doing so reduces the opportunities of your claim being denied or postponed.

If you're covered by life insurance coverage, inform your relative that you have a policy so they don't end up being unclaimed life insurance beneficiaries. Provide your insurance business as much detail as possible about your beneficiaries, consisting of names, addresses and Social Security numbers, to make it much easier for the insurance provider to find them. how long can you stay on your parents insurance.

Some states are putting pressure on life insurance business to pay out unclaimed survivor benefit. Since of this, insurance coverage companies routinely use Social Security data to examine to see if insurance policy holders are still alive. When they learn one passed away, they'll research to look for the beneficiariesThere isn't a time limitation for when you need to file to declare a benefit.

In many circumstances, they should pay the claim within 30 days of approval.Missing Cash has a database that'll help you see if you have an unclaimed life insurance coverage advantages. All you need is the state name of the policyholder and the state they acquired life insurance coverage in. Last Updated: April 17, 2020 When a loved one. how to apply for health insurance.

passes away, one vital task is dealing with financial affairs and funeral arrangements. Life insurance can cover the costs of burial services. It can also decrease the tension of managing a deceased relative's monetary matters during an attempting time. Since 2013, over $1 billion of life insurance coverage policies had gone unclaimed. X Customer Reports Not-for-profit company dedicated to customer advocacy and item testing. Life insurance coverage policies can go unclaimed since it is the household members 'duty to notify the insurance provider when the insurance policy holder dies; the insurance provider will not make an effort to find recipients the company does not even know an insured has actually passed away. Finest Life Insurance Offers For You Conceal Because insurance policy holders frequently have an aversion to speaking about their own death or discussing who's going to inherit cash, recipients might not even understand a policy exists. MIB Solutions, which tries to find policies for beneficiaries through its database of life insurance coverage application data, says that" it is possible, if not most likely, that countless dollars in life insurance goes unclaimed. "That number has actually now reached billions. While some companies have actually already taken on some of the concern, specific states are developing legislation needing life insurance coverage business to make collective effort into notifying the beneficiaries of policies. But if you're unsure whether you're the recipient of a lost life insurance coverage policy, you may be at a dead end if you don't have a copy of the policy.

or understand which business issued it. The ACLI has a variety of tips for those who believe they might be due money from life insurance policies. Browse bank check books and/or canceled checks to see if any were composed to pay premiums. If you find a policy, get in touch with the insurer even if you're uncertain whether.

What Is The Difference Between Term And Whole Life Insurance Things To Know Before You Buy

it is still in force. It's helpful to get in touch with life insurance coverage business directly by using a list from either the state insurance department or Best's Insurance coverage Reports discovered in the majority of libraries. Call the worker advantages workplace at their last and previous locations of employment, or consult the union welfare workplace, if required. Review tax return for the previous two years to try to find interest earnings and costs. Contact any law offices where the departed my have actually been recommended. Examine the mail for as much as one year after death for premium notifications, which are usually sent out annually. However, you might find an annual statement regarding the status of the policy, and even a notice of dividend. If the death is an old one, contact the deceased's state's unclaimed property workplace to see if any cash from life insurance coverage policies might have been turned over to the state. Here the deceased's name is matched against approximately 170 million records. If the insurance policy holder obtained the policy in 1996 or after, you may find it here. Administrators and administrators are entitled to order a report, however in cases where neither is available, a making it through partner or closest relative has the right. Another resource is the National Association of Insurance Coverage Commissioners (NAIC )Life Insurance Policy Locator Service. This is a free service NAIC is providing - what is a premium in insurance. On request per deceased person is all that is needed for this search of all getting involved companies' databases. Among the finest resources may be other family members. After somebody dies , everybody has an interest in seeing his or her affairs settled, especially when there are funeral service expenses to be paid. The National Association of Insurance Commissioners( NAIC) Life Insurance Policy Locator continues to connect customers with lost life insurance. Each year, millions of dollars in life insurance benefits go unclaimed by recipients who can't find their deceased enjoyed ones 'policies.

or in some cases may not even know the policies exist. This totally free online tool, kept by the NAIC, has received 145,432 demands which has led to 46,665 matches of lost or lost life insurance policies or annuities with claim amounts of $650,520,451 million being reported by companies through July 31, 2019 considering that its November 2016 launch." Losing a loved one is frequently an uncomfortable, chaotic.

time. Cioppa, NAIC President and Maine Insurance Superintendent." The NAIC's Life Insurance coverage Policy Locator offers customers a method to easily look for policies and annuities. "The policy locator requests are safe, personal and free. Any matches found by participating insurance providers are reported to state insurance agencies through the NAIC Life Policy Locator.

Anyone. This service is open to the general public, consisting of beneficiaries and legal agents. Generally, a certified death certificate and business declare type should be submitted to the insurance company which found a policy. It might use http://www.timeshareexitcompanies.com/wesley-financial-group-reviews/ up to 90 organization days to receive a response. Please keep in mind a requester will not get an action if no matches are found, the requester is not the recipient, or the requester does not have legal authority to acquire details about the deceased. If you can't find the life insurance policy of a deceased relative, you've probably inspected the apparent locations desk drawers, file cabinets, perhaps even under the mattress. Now it's time to widen the search. You'll require to find the name of the business that released the policy in order to make a life insurance claim. Here are ways to discover it. When you send your paperwork, the following states will forward the information to all life insurers certified there: The insurers will search their records to see if any life insurance coverage policies remain in https://www.topratedlocal.com/wesley-financial-group-reviews the name of the deceased. If so, the life insurance coverage companies will contact you if you're the recipient or departed person's legal agent or administrator.

Examine This Report on How To Cancel State Farm Insurance

Believe you may want irreversible life insurance however can't manage it. Most term life policies are convertible to permanent protection. The due date for conversion varies by policy. Think you can invest your money much better. Purchasing a cheaper term life policy lets you invest what you would have spent for an entire life policy.

In 2020, estates worth more than $11. 58 million per person or $23. 16 million per couple are subject to federal estate taxes. State inheritance and estate taxes differ. Have a long-lasting reliant, such as a child with unique needs. Life insurance can fund a special requirements trust to offer take care of your child after you're gone.

Want to invest your retirement savings and still leave an inheritance or money for final expenditures, such as funeral expenses. Want to adjust inheritances. If you prepare to leave a company or property to one kid, whole life insurance could compensate your other children. If you require lifelong protection however desire more investing choices in your life insurance coverage than whole life supplies, think about other kinds of permanent life insurance coverage.

Variable life insurance or variable universal life insurance both provide you access to direct financial investment in the stock market (how much does long term care insurance cost). Indexed universal life insurance pays interest based on the movement of stock indexes. In addition to the financial investments they provide, all these options can also be more affordable than whole life if the marketplace cooperates.

That can lead to great savings or to unforeseen expenditures. As constantly, discussing your specific needs with a fee-only financial coordinator is an excellent primary step.

Term life is usually less expensive than a permanent whole life policy however unlike irreversible life insurance coverage, term policies have no money value, no payment after the term expires, and no value aside from a death advantage. To keep things easy, a lot of term policies are "level premium" your month-to-month premium remains the very same for the entire regard to the policy.

That benefit is normally tax-free (unless the premiums are paid with pre-tax dollars). You may have seen or heard advertisements that state things like, "A male non-smoker in his 30s can get a 20-year $500,000 term policy for under $30 a month." Some people can get that much protection for under $30 but it's manual.

Not known Details About How To Find Out If Someone Has Life Insurance

This is called the "underwriting" process. They'll normally ask for a medical test to evaluate your health, and need to know more about your occupation, lifestyle, and other things. Certain hobbies like diving are considered risky to your health, which might raise rates. Likewise, unsafe occupational environments for instance, an oil rig also might raise your rates.

The longer your term, the more you'll generally pay monthly for a given protection quantity. Nonetheless, it normally pays to err on side of getting a longer-term policy than a shorter one due to the fact that you just never ever know what the future holds and it is normally easier to get insurance coverage while you are younger and in great health.

Whatever coverage quantity you need, it will likely cost less than you believed: A recent survey found that 44 percent of millennials think that life insurance coverage is at least five times more expensive than the real expense. 1 Who gets the benefit when you pass away? It does not all have to go to someone. how long can children stay on parents insurance.

And while beneficiaries are normally family, they do not have to be. You could choose to leave some or all of your advantages to a trust, a charitable organization, or perhaps a pal. As you shop around and start speaking to business or insurance representatives you may hear about various sort of term policies.

Likewise called level term; this is the simplest, most typical kind of policy: Your premium remains the very same for the whole term.: Likewise called an annual eco-friendly term. This policy covers you for a year at a time, with a choice to renew without a medical examination for the duration of the term however at a greater expense each year. how much does home insurance cost.

This kind of term policy actually repays all or a part of your premiums if you live to the end of the term. What's the catch? Your premiums could be 2-4 times greater than with a level term policy. Likewise, if your financial status changes and you let the policy lapse you may only get a part of your premiums returned or absolutely nothing at all.

This also implies that the insurance provider has to assume that you are a dangerous possibility who has health concerns, so your premiums may be much higher than they otherwise would be. Likewise, the policy may not pay a full survivor benefit for the first couple of years of coverage. If you have health issues but are able to handle them, it will normally be worth your while to get a traditional term life policy that is underwritten (i.

The 20-Second Trick For How Much Term Life Insurance Do I Need

Convertibility is a policy arrangement that lets you change your term insurance into a irreversible entire life policy later on without having to get a new medical examination. It's a feature offered by practically all significant insurance coverage business that let you alter https://www.yelp.com/biz/wesley-financial-group-nashville-3 your type of life insurance coverage. Guardian, for instance, lets you convert level term insurance coverage at any point in the first 5 years to a long-term life policy and even uses an optional Extended Conversion Rider which lets you do so for the period of the policy.

Another factor: you're brought in to the cash value element of an entire life policy. Or possibly you want irreversible life-long protection. A term policy might well be your finest choice now, however things can alter. Search for an insurance company that offers the alternative to transform from term to an entire life policy without taking another medical examination, which would likely increase your expense.

Generally, lower than entire life Usually, 6x 10x more pricey than term for the same death benefit; but as cash value constructs it can be used to supplement premiums. Renewal expense boosts with age Cost remains the very same for life No Yes Normally, 10 thirty years Life time protection (as long as payments are made) Can be level or boost over the length of the policy Level remains the very same monthly In many cases In many cases No Yes expense can be offset as cash value constructs (usually after 12+ years) No Yes builds up over time 3 No Yes withdrawals and loans Have a peek here are enabled (however if unrepaid, this will diminish the policy values https://www.crunchbase.com/organization/wesley-financial-group and death advantage) Yes Yes Reasonably easy More complicated If you have a young family, it will take lots of years of earnings to pay to feed, house, outfit, and educate your children through to their adult years.

Here are a few general rules individuals utilize to assist determine just how much they require:: This is among the simplest guidelines to follow, and it can supply a beneficial cushion for your household however it doesn't take all your actual expenditures and needs into account. If you add $100,000 - $150,000 for each kid, that can assist ensure they can achieve more of the opportunities you desire for them.

The Definitive Guide to How Much Does Motorcycle Insurance Cost

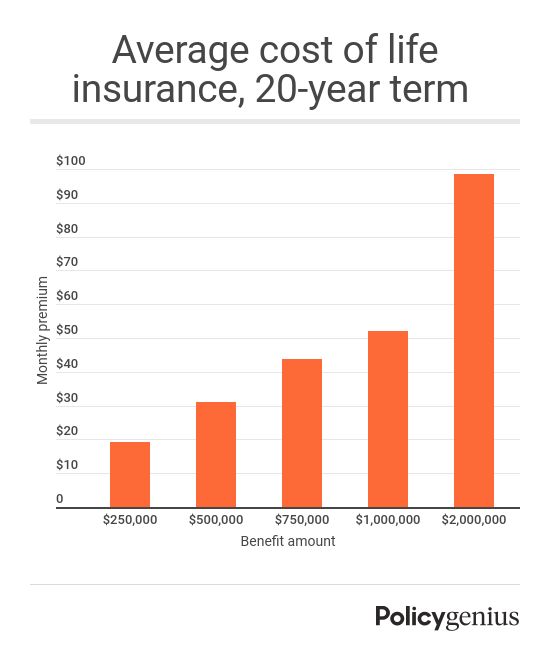

Health profile and level term lengthAge 30Age 40Age 50Age 60Female non-smoker 10-year term$ 223$ 306$ 573$ 1,184 Female non-smoker 20-year term$ 314$ 477$ 955$ 2,310 Female non-smoker 30-year term$ 431$ 695$ 1,537$ 7,300 * Female smoker 10-year term$ 439$ 692$ 1,482$ 3,072 Female smoker 20-year term$ 669$ 1,185$ 2,386$ 5,219 Female smoker 30-year term$ 915$ 1,655$ 3,695$ 13,030 * Male non-smoker 10-year term$ 263$ 358$ 735$ 1,716 Male non-smoker 20-year term$ 368$ 565$ 1,226$ 3,128 Male non-smoker 30-year term$ 528$ 872$ 2,023$ 7,300 * Male smoker 10-year term$ 553$ 866$ 1,970$ 4,424 Male cigarette smoker 20-year term$ 826$ 1,487$ 3,177$ 7,100 Male smoker 30-year term$ 1,166$ 2,140$ 4,470$ 13,030 ** Restricted quotes offered. Information source: Compulife Quotation System since August 2020.

You may not be able to stop aging, but you can absolutely stop cigarette smoking. After five years, you can likely certify for non-smoker rates. You do not have to be a smoker to get cigarette smoking rates. Anything that provides nicotine into your system, from nicotine spots to e-cigarettes, will amass you greater life insurance rates.

Ellis recommends that it's an excellent concept to get life insurance coverage as quickly as somebody else depends on your income. "This might be when you and another person sign a lease together or purchase a car/home. Or Homepage it might be whenever you have kids. If one partner is 'remain at house,' I would still advise they buy some life insurance.

When your dependents are financially steady, you need to drop your life insurance except for perhaps a little amount to spend for a funeral," Ellis includes. Expenses can rise quick when you take care of a household, pay a home loan, prepare for college and all of the other elements involved in your financial resources.

What Is E&o Insurance - Questions

com. "It's a time in life when you have a substantial amount of living expenditures and financial obligation. Raising your term amount when you are young and healthy is economical and a good concept, since the rates will increase considerably as you age." When you make an application for term life coverage, you'll be asked concerns about your individual health history and family health insurance coverage.

Do not be amazed if you're asked the exact same set of concerns more than as soon as very first by your agent and after that by the paramedical professional who performs the exam. Some brand-new insurers are using instant-approval policies where a medical exam is not needed however still provide high policy limits. Likewise, some popular life insurance coverage companies are using same-day approval policies.

Choosing the best term life policy requires a little investment of time, but the advantages can be priceless. The first factor for this is obvious: The right policy will help look after your recipients in case you pass away. However the second reason, which will benefit you even if you outlast your life insurance policy, is the comfort that comes with knowing that you and your loved ones are covered.

Utilize the life insurance coverage calculator to find just how much coverage you should have. A life insurance coverage calculator takes into account your funeral service expenses, home loan, earnings, financial obligation, education to give you a clear price quote of the perfect quantity of life insurance protection. 2. Picking a life insurance coverage company. Guarantee. com maintains a list of the finest life insurance coverage companies based upon client evaluations, making picking a reliable insurer much easier.

How How To Start An Insurance Company can Save You Time, Stress, and Money.

Choosing the length of the policy. Common terms consist of five, 10, 15, 20 and 30 years. 4. Selecting the amount of the policy. This is the sum your recipients will receive in the event of your death. The quantity you select should depend upon a number of aspects, including your earnings, debts and the number of people who depend on you economically.

5. Medical examination. The exam typically covers your height, weight, high blood pressure, case history and blood and urine testing. 6. Initiation of policy. When your policy remains in location, keeping it refers paying your regular monthly premiums. From there, if you die while the policy is in force, your recipients get the face quantity of the policy tax-free.

Term life insurance coverage, likewise referred to as pure life insurance, is a type of life insurance coverage that ensures payment of a mentioned death advantage if the covered individual dies throughout a specified term. As soon as the term expires, the insurance policy holder can either restore it for another term, convert the policy to permanent coverage, or enable the policy to end.

These policies have no worth besides the guaranteed death advantage and feature no cost savings component as discovered in a whole life insurance item. Term life premiums are based upon a person's age, health, and life span. When you buy a term life insurance policy, the insurance company identifies the premiums based upon the worth of the policy (the payment amount) as well as your age, gender, and health.

Not known Facts About How Do Life Insurance Companies Make Money

The insurer may likewise ask about your driving record, existing medications, smoking cigarettes status, profession, pastimes, and family history. If you die throughout the term of the policy, the insurance provider will pay the face value of the policy to your beneficiaries. This cash benefitwhich is, in the majority of cases, not taxablemay be utilized by recipients to settle your health care and funeral expenses, customer debt, or home loan financial obligation to name a few things.

You might have the ability to restore a term policy at its expiration, but the premiums will be recalculated for your age at the time of renewal. Term life policies have no worth besides the ensured survivor benefit - how much is car insurance a month. There is no savings element as found in Click here for more a entire life insurance coverage item.

A healthy 35-year-old non-smoker can usually get a 20-year level-premium policy with a $250,000 stated value for $20 to $30 monthly. Acquiring a whole life equivalent would have significantly higher premiums, possibly $200 to $300 per month. Because a lot of term life insurance policies expire prior to paying a survivor benefit, the general danger to the insurer is lower than that of a permanent life policy.

When you think about the quantity of protection you can get for your premium dollars, term life insurance tends to be the least costly choice for life insurance. Rates of interest, the financials of the insurer, and state guidelines can likewise impact premiums. In basic, business often offer better rates at "breakpoint" coverage levels of $100,000, $250,000, $500,000, and $1,000,000.

A Biased View of What Does Long Term Care Insurance Cover

He purchases a $500,000 10-year term life insurance policy with a premium of $50 each month. If George passes away http://elliotvkbo852.wpsuo.com/how-to-get-cheap-car-insurance-can-be-fun-for-everyone within the 10-year term, the policy will pay George's beneficiary $500,000. If he passes away after he turns 40, when the policy has ended, his recipient will get no benefit. If he renews the policy, the premiums will be higher than with his initial policy due to the fact that they will be based on his age of 40 instead of 30.

Some policies do provide ensured re-insurability (without evidence of insurability), but such functions, when offered, tend to make the policy cost more. There are numerous various types of term life insurance coverage; the best option will depend upon your individual situations. These supply coverage for a specified period varying from 10 to thirty years.

Because actuaries should represent the increasing expenses of insurance coverage over the life of the policy's effectiveness, the premium is relatively greater than annual eco-friendly term life insurance coverage. Annual renewable term (YRT) policies have no specified term, but can be restored each year without offering proof of insurability. The premiums change from year to year; as the insured individual ages, the premiums increase.

The Buzz on What Is Life Insurance Used For

More junior representatives can frequently advance in making possible and obligation if they want to do so, as they gain more experience in the industry. However the crucial thing to keep in mind about being a life insurance coverage agent is this: When you're a life insurance agent, you're not just offering an item. In later years, the representative may receive anywhere from 3-10% of each year's premium, likewise referred to as "renewals" or "trailing commissions." Let's look at an example: Bob the insurance coverage representative sells Sally a whole life insurance coverage policy that covers her for the rest of her life as long as she continues to make her premium payments.

The policy costs Sally $100 monthly or $1,200 annually. Hence, in the first year, Bob will make a $1,080 commission on offering this life insurance policy ($ 1,200 x 90%). In all subsequent years, Bob will make $60 in renewals as long as Sally continues to pay the premiums ($ 1,200 x 5%).

As pointed out previously, a life insurance representative is not an occupation for the thin-skinned or faint of heart. In truth, more than any other element, consisting of education and experience, life insurance agents must possess a fighting spirit. They need to be individuals who like the excitement of the hunt, the rush of a sale, and see rejection as a stepping stone to eventual success.

The huge majority of life insurance companies have no official education requirements for becoming a representative. While many prefer college graduates, this general rule is continuously neglected in favor of the "right" prospects. Previous experience in the insurance market is not required since a lot of medium and big insurance carriers have internal programs to train their salespeople about the items they're going to sell.

Insurance coverage representatives are currently accredited by the private state or states in which they'll be offering insurance coverage. This normally requires passing a state-administered licensing examination along with taking a licensing class that usually runs 25-50 hours. The sales commission life insurance coverage agents might earn in the first year if they are on a commission-only salary; that's the greatest commission for any kind of insurance coverage.

Primarily, you'll require to put together a resume that highlights your entrepreneurial spirit. how to become a life insurance agent. You'll desire to consist of anything that shows you taking initiative to make things occur, whether it was beginning your own company or taking somebody else's service to the next level. Life insurance coverage agents need to be driven and have the ability to be self-starters.

How Much Does A Life Insurance Agent Make A Year for Beginners

When you've got your resume polished, Browse around this site you'll wish to start finding positions and using. It's actually important you do not feel forced to take the very first position that occurs, as working for the wrong business can both burn you out and haunt you for the rest of your insurance coverage profession.

Possibly the best place to start in choosing where to use is to check out the insurance provider ranking sites for A.M. Best, Moody's, or Requirement & Poor's. From there, you'll be able to develop a list of business that have ratings of "A" or greater in your state. These business will usually offer the most-secure products at reasonable rates, with an emphasis on compensating and keeping quality representatives.

Once you have actually produced this list, start taking a look at each business. Due to the high turnover rate of insurance coverage agents, many business prominently publish their task listings by geographical location, that makes them quickly searchable for you. When you find a business in your area that appears to fit your personality, obtain the position as the business advises on its site.

Lots of insurance coverage company recruiters will not even interview a possible representative who http://riveroarf897.yousher.com/not-known-details-about-how-to-find-out-if-a-deceased-person-had-life-insurance doesn't first make a follow-up call, due to the fact that this is a strong indicator of a prospective agent's tenacity. Throughout your interview, continue to communicate your entrepreneurial and "never state stop" personality, because a lot of supervisors will employ somebody based upon these aspects over all the others combined.

Your sales manager will be the very first to remind you that your only function in life is to discover possible clients. In fact, they'll be even more thinking about how numerous contacts you're making each week than how well you know their product line. Do anticipate to have a hard time financially for the very first few months until your very first sales commissions start rolling in.

Lots of representatives are now fortunate to be made up for one to two months of training before being put on a "commission-only" basis. While the life insurance industry promises great benefits for those who are ready to strive and endure a good quantity of ca cuoc the thao keo chau a rejection, there are 2 other mistakes you need to be knowledgeable about.

Not known Facts About What Does It Take To Become An Insurance Agent

While that might be appealing and look like a terrific concept to get you started, it can also burn a great deal of bridges with people you care about. Second, you need to visit your state insurance commissioner's website and have a look at the problem history versus companies that you're thinking about working for.

Accepting a task with the wrong insurer will go a long way toward burning you out and destroying your imagine a promising career. If a profession in life insurance coverage sales is something you genuinely desire, take your time and await the best opportunity at the best company.

Insurance is too intricate. I'm not qualified. It's far too late to change professions. If you've ever thought about the actions to ending up being an insurance agent, you have actually likely been exposed to these typical misunderstandings and mistaken beliefs about selling insurance. To set the record straight, Farm Bureau Financial Solutions is here to bust the leading misconceptions about ending up being an insurance coverage agent and help guarantee nothing stands in between you and your dream chance! The fact is, most of our agents don't have a background in insurance sales.

Though a number of our top candidates have some previous experience in sales, company and/or marketing, particular characteristic, such as having an entrepreneurial spirit, self-motivation and the ability to communicate successfully, can lay the best foundation for success in ending up being an insurance representative. From here, we equip our agents with focused training, continuing education chances and one-on-one mentorship programs designed to assist them find out the ins and outs of the industry.

Farm Bureau agents discover their profession path to be satisfying and rewarding as they assist individuals and households within their community safeguard their livelihoods and futures. They comprehend that their business is not almost insurance products - it has to do with people, relationships and making whole neighborhoods healthier, more secure and more safe.

Our group members are trained on our sales procedure which will assist them figure out the best coverage for each client/member or company. The Farm Bureau sales procedure begins with identifying a possibility, whether you're selling a personal policy or a business policy. From there, you can get to understand the prospective client/member, discover their requirements and determine their long-term goals.

The 5-Minute Rule for What Happens To Life Insurance With No Beneficiary

This means insurance coverage business submit their "rate list" of all the policies they offer with the state's insurance coverage department. This guideline means a representative selling you an insurance coverage policy can't estimate a higher price than if you 'd just gone directly to the business itself. That's why it's wise to get a variety of quotes from a representative.

Insurance coverage representatives fall under 2 types captive or independent. The distinction in between the two is how far they can reach into the life insurance market. Captive insurance coverage representatives are only able to offer insurance on behalf of the company they work for. They have great understanding of the policies used but are limited since of being captive to that company alone.

That suggests noncaptive representatives can discover and offer insurance from a much larger swimming pool of life insurance coverage service providers. Which benefits you due to the fact that they can save you money on your premium (which is the quantity you pay monthly or annually for your life insurance coverage.) So, you have actually made the call and are speaking with a representative.

Are they listening well about who you are and what you need coverage for? Ensure they're not attempting to oversell things to you. Life insurance is made complex enough without them evading your questionsno matter how unimportant they seem. If they're pressing you to decide on that very first call, it's prematurely! They shouldn't withhold this information, in addition to just how much commission they're paid, either.

You can be prepared by knowing what they indicate, but if they're still attempting to sell you a bunch of stuff you world financial group wfg hear my story don't require (or are just a bad listener), they're not doing their job! It's always a good idea to utilize an expert when it pertains to buying life insurance coverage.

It fasts and easy to use and offers you something to deal with when you're speaking to a representative. Dave constantly recommends choosing independent insurance representatives. They can shop around a bigger market to get the best choice for Discover more here you, saving you time and money. Our relied on friends at Zander Insurance have been assisting individuals similar to you get the finest life insurance prepare for decades.

By Ashley Donohoe Updated June 28, 2018 Independent insurance coverage agents run their own services and they can pick which insurance brokerages they wish to deal with. These representatives use their proficiency to help their customers discover the insurance plan that fit their needs and spending plans. This holds true whether the agent's clients need health, automobile, property, timeshare out life insurance or any other type of insurance.

All about How To Find A Good Insurance Agent

You'll have greater flexibility in picking your own insurance coverage items. How much independent insurance coverage representatives make varies by the number of customers they have; what types of clients and how numerous insurance coverage products their clients buy; and what the commission structure resembles for the brokerages they deal with. Independent insurance agents are considered entrepreneur who can use insurance items from a range of providers to their clients.

They offer customers with customer care, including giving information about particular policies, assisting with the policy choice process, getting clients signed up for insurance coverage and helping them renew their policies as needed. When working with consumers, be confident and persuasive so that you motivate your clients to buy what you're offering.

You can start working as an independent insurance coverage representative with a high school diploma; however, earning a degree associated with business can offer you with beneficial company and sales skills. You likewise need to end up being certified in your state for you to be able to offer the kinds of insurance products you want; often, this needs taking insurance coverage courses and passing tests.

After you're accredited, guaranteed and registered, you can begin contracting with insurance brokerages to offer products to your clients (how to become an independent insurance agent). The average yearly wage for all insurance representatives in May 2017 was; earnings were less for the lower half of agents and greater for the top half, reported the Bureau of Labor Data.

Insurance carriers used a typical wage of, whereas insurance coverage companies and brokerages used a somewhat lower average wage of. Employing majority of insurance representatives, insurance agencies and brokerages are the leading companies. Around 18 percent of insurance representatives are self-employed, whereas a smaller variety of representatives work for insurance coverage providers.

A great deal of your time will be invested calling customers via phone or internet in a workplace or traveling to satisfy them in person. This position generally requires that you work full-time at this venture; you might also find that you require to work additional hours to manage documentation and marketing.

When you first start, you'll require to construct a client base to earn a consistent income, which typically originates from your commission from the products you've sold. Over the years, as you construct your customer base, get experience, and market yourself, you can anticipate to make more money. PayScale reported that an independent insurance coverage representative's salary ranged from $24,658 to $62,629 (consisting of bonuses and commissions) in April 2018.

The smart Trick of How To Get An Insurance Agent License That Nobody is Discussing

Independent insurance coverage representatives have good job potential customers, since it is more inexpensive for insurer to work with them. Although consumers tend to seek insurance alternatives online, independent representatives are needed to help clients select the right choices and to provide info about policies. To maximize your potential customers, you can sell medical insurance, which remains in high need.

It's not a surprise that offering life insurance is such a popular profession. With over 1 million insurance agents, brokers, and service staff members in the united states in 2020, it stays one of the largest industries. One of the advantages of selling life insurance coverage are the versatile hours. You can do it on the side initially and earn a fantastic living if you are willing to put in the work.

It includes making phone calls, setting consultations, following up, and getting told NO. If this does not seem like nails on a chalkboard to you, then chances are you have the right personality for offering life insurance. Like any profession, it requires time to get experience and develop your earnings.

Lots of make a lot more than that! You can expect to earn $2,000-5,000 per month starting out. This will depend upon the products you offer, the commissions, and how hard you are prepared to work. Many agents nowadays opt to offer items from the best life insurance companies. See this page to learn about no exam life insurance.

Many representatives get going in insurance as a "side hustle". They frequently spend time at nights networking to make sales. Once you get a license and agreement, start connecting. Buddies, close family members, and members of their neighborhood are a fantastic method to get sales. Quickly you will see the chance for what it is and might select to devote to selling insurance coverage full time.

I suggest ExamFX, and their self-study course is $149. 95 in the state of Georgia. You will have 60 days to finish the course and pass the simulated exam. Once completed, you will receive your certificate. To take the state exam, you will require the certificate. The state exam in Georgia is $63.

Indicators on How To Be An Independent Insurance Agent You Should Know

Many insurance business permit you to get a quote online, where you send your state, gender, birthday and desired protection quantity, and get an instant rate. You can even purchase a policy on the spot. As long as you continue to pay the premiums, your policy remains in effect. Each time you pay your premium, the insurer allocates some of that cash into your cash value account that is invested and grows overtime.

When you die, your beneficiaries will receive the survivor benefit, assuming the policy has actually been active for a minimum of 2 years. As an option, you can likewise designate a funeral home as the recipient so the cash goes straight towards your funeral service expenses. Guaranteed life insurance coverage policies have a pretty low survivor benefit cap, which is generally around $25,000. Guaranteed concern life insurance protection tends to be expensive.

To help you identify a typical rate for ensured problem life insurance, we received numerous sample quotes for a 70-year-old woman living in California, with $25,000 in protection. Here are the rates we got: $204 each month $175 per month $186 monthly Surefire life insurance coverage premiums are solely based upon your state, age, gender and the quantity of coverage you desire.

Furthermore, some states are more expensive for life insurance than others. The only method to determine how much you'll pay is to get a personalized quote. If you're on a spending plan, guaranteed life insurance coverage may not be the very best choice for you. A better choice would be simplified entire life insurance.

There are a number of advantages to guaranteed life insurance. Initially, it's guaranteedit's nearly difficult to get denied protection, even if you have multiple health dangers. It's quick and easy to get protection, and there's no waiting period for approval. The other significant benefit is that guaranteed life insurance assists cover end-of-life expenditures, so your loved ones don't have to pay any out-of-pocket costs.

The premiums are exceptionally expensive, and you don't get much in return. Most insurer cap the survivor benefit at $25,000. While that's normally enough to cover funeral expenses, it's inadequate to financially support your loved ones for the future. Despite the term "ensured," it is possible (although not likely) that you could get rejected coverage.

There is likewise an age cap. If you're 80 or older, you most likely can't get a new policy. So, is ensured life insurance worth it? Yesbut only for some people - what is term life insurance. Prior to you buy guaranteed life insurance coverage, you must request conventional life insurance coverage initially. Surefire protection needs to only be utilized as a last resort option.

4 Simple Techniques For What Type Of Insurance Offers Permanent Life Coverage With Premiums That Are Payable For Life

Every company provides slightly various rates and protection quantities. If you're thinking about an ensured life insurance policy, do some research study to find a company in your area that offers the quantity of coverage you desire, has great consumer service reviews, and is financially strong. The rate of guaranteed life insurance coverage is various for everyone.

The older you are, the more you'll spend for insurance coverage. Higher coverage quantities also equate to a more costly rate. A lot of insurance coverage companies just sell ensured problem coverage to people between the ages of 50-80, although the specific age range might vary a little.

Life insurance is developed to provide some financial security to your enjoyed ones after you're gone. Depending upon your situation, the cash can help pay off debt, fund your partner's retirement or assist your kids pay for their education. There are numerous different types of policies to select from. If you don't know the truths, it might spell monetary catastrophe for those you leave behind.

There are two basic types of life insurance: term and permanent. Term policies pay out a specific survivor benefit and remain in location for a set period of time. Term life insurance can typically be acquired for a 5, 10, 15, 20 or 30-year term. Irreversible life insurance coverage on the other hand stays in impact throughout your life.

A whole life insurance coverage policy enables you to build cash value that you can draw against later. Universal and variable life policies are tied to different types of financial investment cars. When choosing in between permanent and term life insurance coverage, you'll require to evaluate what you truly want from the policy.

For example, if something occurs to your spouse and you only need enough to cover mortgage or credit card payments, a term policy might make the most sense. However maybe you're trying to find a policy that will enable you to make some returns on your financial investment. If you do not mind paying a little bit more, you may desire to check out an irreversible policy.

In this manner you can discuss what is essential to you (retirement, paying https://www.linkedin.com for a kid's college education, and so the timeshare on) in the context of making certain you have the ability to fulfill those goals for your household even if something happens to you. In addition to choosing a policy type, you also have to choose just how much of a death benefit you require.

The Ultimate Guide To What Is Direct Term Life Insurance

If you do not do your homework, you risk of offering your beneficiaries short in the future. You'll wish to consider numerous factors when calculating how much life insurance coverage you require. These include your age, general health, life span, your earnings, your debts and your assets. If you've currently developed a large savings and you don't have much debt, you may not require as much protection.

You will also wish to avoid ignoring the value of a non-working partner. When it comes to their death, you won't require life insurance coverage to replace lost earnings. Nevertheless, that money can still help cover new expenses like kid care or housekeeping aid. Like any other kind of insurance coverage, you'll desire to go shopping around to make sure you're getting the very best rate.

When you're taking a look at several plans, you wish to ensure you're offering the very same information to each insurer. You also desire to evaluate the various policies to try to find any significant distinctions in the protection. This helps to ensure you're getting the most accurate quotes. Sometimes, the cost of purchasing life insurance coverage might suffice to terrify you away.

But life insurance coverage is not something you can afford to stint. Looking at your out-of-pocket expenses is a more instant concern. You'll require to believe about whether the cash you conserve now is really worth the affect it could have on your family when you're gone. If you're discovering that life insurance is too costly, you may require to have a look at your budget plan.

The sooner you purchase life insurance, the much better. Premiums will just increase as you age. Even if you're in relatively health, you'll still pay more for each year you put it off. Not only that however you likewise run the risk of establishing a serious illness or disease which might lead to much higher premiums or being rejected protection entirely.